Today we are going to look at a company of the entertainment sector. More specifically, the video game sector. This is Activision Blizzard, the largest creator of video games for third-party platforms. It has titles as well-known as Call of Duty, Candy Crush or World of Warcraft. Let’s take a closer look.

Introduction

Origins

The video game industry is considered to be born in 1972 with the company Atari, and in 1977 its first video game console was sold on a massive scale: the Atari 2600. It was an early era when Intel had barely developed its first microprocessor.

Shortly after, in 1979, Activision was born with the idea of developing video games for the successful Atari 2600. Although the world of video games was still in an early stage, Activision was one of the first companies to realize the promising potential of this industry, and had the idea of developing video games taking advantage of the success of companies like Atari, who managed to successfully launch their platforms. It was the first company of what we know today as «3rd Parties», companies that develop entertainment software for other companies’ videogame consoles.

In fact, Activision was founded by some programmers from Atari itself, dissatisfied with the little recognition received after the success of their work. As there were no «3rd Party» companies at that time, there was no restriction to develop video games for other companies. And these programmers took advantage of this loophole. They formed the name Activision by intertwining the words «Active» and «Television», and quickly achieved great success with video games for the Atari 2600 console such as «Kaboom!» and «Pitfall! . These games were even more successful than Atari’s own video games. Because of this, they had to face serious lawsuits from their former employers, but the American justice recognized the «3rd Party» model only by forcing Activision to pay some royalties to Atari.

However, this recognition of the «3rd parties» by the courts led to the appearance of many competitors on the market. Many programmers began to develop video games, and this caused an earthquake for young Activision. Video games were selling in droves, and this oversupply made Activision slash its prices. The company suffered greatly and this crisis caused a huge contraction of the company: even the founders themselves left it.

Activision tried to escape the video game console crisis by buying in 1986 the competitor Infocom, which developed video games for PC. In 1988 it even changed its name to Mediagenic, in order to enter the PC business software sector. However, none of this worked and after several years of losses, and with a hefty debt, the company seemed doomed to disappear.

Although everything indicated that 1991 would be the last year of the company’s existence, its savior appeared: Bobby Kottick. He was a brilliant entrepreneur, who a few years earlier had been counselled by Steve Jobs himself on leaving college to focus on software development. Kottick’s work had impressed Steve Jobs, but he thought the company Kottick headed was too small. Kottick was also passionate about the video games industry. Therefore, after unsuccessfully trying to acquire some other companies, he ended up acquiring, together with his partner Brian Kelly, an important part of the almost bankrupt Mediagenic. And this acquisition was only about purchasing what the company itself had despised not long ago: its name, Activision, that is, its reputation in the video game industry. Kottick became CEO, and they quickly changed the company’s name back to Activision, to put the company’s bad times behind it.

Kottick successfully restructured the company, paying off some debts to its distributors in Activision stock to get them more involved, leveraged deals with Sega and Nintendo to develop games, and the company rapidly expanded into various markets such as Australia and the UK acquiring a multitude of game development studios. In 1993 the company went public, where it started trading for just $1.25/share.

In 1996 Activision was already profitable again and began a busy period of acquisitions, including Neversoft (creator of the Tony Hawk video games); Infinity Ward (creators of Call of Duty); Treyarch (studio that supported the development of the following games of the Call of Duty and Tony Hawk franchises); RedOctane (creators of the GuitarHero video game) among many others. All these acquisitions were made between 1997 and 2008. During this period, Activision also signed many agreements with Marvel, Disney, LucasArts, Viacom or Sony, which allowed it to develop videogames with characters developed by these companies such as Star Wars, Spiderman, X-Men or Star Trek on the new successful platforms, such as Sony’s PlayStation.

However, while all of these acquisitions and deals were successful, they were based on game franchises that generated a one-time payment and did not leverage the emerging trend in the gaming world: online gaming experience. An online ecosystem of players could create subscription payments and small recurring transactions.

Therefore, in 2008 Kottick contacted the French multinational Vivendi, which had a video game division that included the studios Blizzard Entertainment and Sierra Entertainment. After arduous negotiations, and with Activision under pressure from the gradual loss of luster of its star franchises, it agreed to Vivendi’s demands: to merge the two companies, but with Vivendi as majority shareholder with 52% of the shares of the new company, which would be called Activision Blizzard.

With this merger, Activision Blizzard would have the World of Warcraft video game franchise, which already had an established online multiplayer ecosystem and generated considerable subscription revenues. This merger would make Activision Blizzard the largest 3rd party company in the world, ahead of its direct rival Electronic Arts.

Activision Blizzard bought back its entire stake from Vivendi between 2013 and 2015, but at the same time another giant in the world of video games entered the company’s capital: Tencent Holdings. This Chinese company owns 100% of Riot Games (League of Legends), 40% of Epic Games (Fortnite) and 5% of Ubisoft (Assassin’s Creed) among many others. However, both Tencent’s stake and that of Bobby Kottick and Brian Kelly have been diluted over time.

Since 2015 Activision Blizzard is part of the S&P500 and has reaped several successful video games such as Skylanders (2011-2016) in which it mixed physical figurines with video games or the Destiny and Diablo game sagas. Also in 2016 they acquired the company King for $5.9 billion, developer of the Candy Crush mobile video game. This allowed Activison Blizzard to strongly enter the cell phone platform and the Chinese market. The same year, Activision Blizzard launched the first Overwatch game, a multiplayer shooter that quickly garnered quite a success.

As of today, the company’s top video game franchises are by far Call of Duty, World of Warcraft and Candy Crush.

Recently, the company has suffered numerous scandals, which had a severe impact on its share price. Apparently, the video game industry is a sector in which cases of labor disputes due to poor conditions are not uncommon. Without going any further, Activision Blizzard’s French competitor, Ubisoft, has recently had many lawsuits in this regard.

However, Activision Blizzard has been accused of going even further: it has suffered several allegations of gender pay inequality and several cases of sexual harassment. One of them even allegedly led to the suicide of a female employee. These serious accusations were fueled when some managers, including some women, publicly took a stand with the company denying everything and claiming that the complaints were «distorted or false». However, up to 20% of the workers signed the complaints, which shows the strong fracture that currently exists inside the company between management and workers.

Moreover, Bobby Kottick reacted late to all this turmoil and, although he promised to take action on the matter, the first thing he did was to hire some consultant companies that are famous for confronting workers and preventing them from unionizing. The longtime boss of Activision Blizzard then vowed to leave the company if he fails to address these serious problems of corporate culture and conduct. Many shareholders have openly called for his dismissal and the SEC has an ongoing investigation to assess his level of involvement in the crimes that have occurred.

All these internal labor disputes are especially important in creative sectors such as video games, since creativity depends to a large extent on the talent of its employees. Let’s not forget that Activision itself was founded thanks to some disgruntled Atari employees.

However, all these issues calmed down since the announcement of the company’s last big milestone: its acquisition attempt by Microsoft. In January 2022, the company founded by Bill Gates announced that it had reached an agreement with Activision Blizzard to buy the company for $95 per share: a 45% premium to Activision Blizzard’s share price at the time. The total takeover offer amounted to an exorbitant $68.7 billion, which would be the largest acquisition in the technology sector in history. In addition, a few weeks earlier Warren Buffett had bought Activision Blizzard shares for his Berkshire Hathaway holding company, accumulating almost 2% of the company’s shares. According to Buffett himself, a great friend of Bill Gates, this purchase was made without any knowledge of the acquisition. Moreover, throughout 2022 and with this acquisition by Microsoft already being public, Warren Buffett has been increasing his stake to almost 10% of the company, and has become its main shareholder. He owns these shares at an average of $77 per share.

This is very indicative, given that when the acquisition was made public, Activision Blizzard’s stock jumped from $66 to $81 per share, a value still far from the $95 at which Microsoft has committed to buy it if regulators allow the acquisition. This is because it is not yet clear that the various antitrust regulators in different countries will allow the merger of these two video game titans. The rationale behind this opposition to the merger is that, if they allow it and Microsoft subsequently decides to make Activision Blizzard’s games exclusive to its Xbox platform, then its competitors could be severely affected. The most affected player would be Sony, given that Call of Duty is one of the best-selling games for their Playstation platform. Microsoft has already publicly stated that this is not their intention, but it remains to be seen whether regulators will believe it and finally allow the acquisition. In particular, the last major opposition has been made by the European Union regulators, who have launched an in-depth investigation into whether they should approve this acquisition, and whether in doing so they would not be compromising the competitiveness of the industry. The U.S. Federal Trade Commission (FTC) has also expressed some doubts about the operation and will try to prevent the transaction in court. The latest rumors say that, in order to soften the operation, Microsoft is willing to offer Sony a 10-year contract for the permanence of Call of Duty on the Playstation platform. And the same will be offered to Nintendo, so that Call of Duty can also be played on Nintendo Switch. We will see how it all turns out.

In any case, it looks like Warren Buffett is betting that the acquisition will eventually go through. Although surely, he also believes that buying Activision Blizzard at $77 wouldn’t be a bad investment, in case the authorities prevent the merger.

In any case, let’s analyze Activision Blizzard’s business and see if we agree with the Oracle of Omaha in our conclusions.

Business

Today Activision Blizzard is considered the largest «3rd Party» in the world, only after the Chinese conglomerates Tencent and Netease (which have video game divisions with higher sales), and is in direct competition with Electronic Arts. Sony, Nintendo and Microsoft have a much higher turnover, but are not considered 3rd Parties since they own the most popular video game consoles on the market: Nintendo Switch, Playstation and X-Box respectively.

Activision Blizzard details its Sales in three segments:

- Activision: This division’s flagship game is Call of Duty, one of the most popular militar shooter video games on the market.

- Blizzard: This division manages the Battle.net online platform, from which Blizzard and Activision video games are distributed. Blizzard’s most successful franchises are World of Warcraft, a massively multiplayer online game set in a fantasy world; Hearthstone, an online collectible card game; Diablo, a role-playing fantasy game; and Overwatch, a multiplayer action game.

- King: The flagship franchise of this division is Candy Crush, the famously addictive cell phone game.

- Other: This division includes all businesses that do not fit into the other segments, such as warehousing, logistics and distribution services in Europe for video games of other companies.

Forty-nine percent of Activision Blizzard’s sales come from the USA, with the american continent accounting for 56% of sales. The rest come mainly from France, UK, Germany, Italy, Japan, South Korea, Australia and China. In the Asian giant, an important part of the sales (around 3% of the total) came from the agreements that Activision Blizzard has had for more than 14 years with Netease for the distribution of Blizzard’s video games. However, this agreement ends in January 2023 and it has recently been announced that the parties will not be renewing it. This will mean that games such as Overwatch2, Starcraft and World of Warcraft will no longer be playable from China. We will see if this decision is permanent, or if at some point it will be renewed with Netease or with a competitor like Tencent. In any case, this decision will not be dramatic for Activision Blizzard since the company is well diversified geographically.

Traditionally, selling video games meant selling a game (physical or digital) at a fixed price so that the customer could enjoy it entirely. Activision Blizzard calls this «Product Sales» in its Income Statement. However, currently the company’s business model is to promote subscriptions and in-game micro-transactions, instead of the single sale of a video game. For example, buying new weapons or exclusive avatars (Call of Duty), paying for subscriptions to play online (World of Warcraft) or paying for more lives or to skip a game level (Candy Crush). Activision Blizzard calls these micro-transactions «In-Game, subscription and other Revenues», and they already represent 74% of the company’s Sales. This category also includes sales from licensing and advertising in video games. Also, the vast majority of the company’s sales are produced in online channels.

As major shareholders, we find Warren Buffett’s conglomerate, Berkshire Hathaway, ahead of the rest. It currently holds 7.69% of the shares, having recently divested part of the shares following the doubts raised by European and UK regulators about the acquisition by Microsoft. Other major shareholders include The Vanguard Group (7.42%), Blackrock (4.76%) and State Street (3.86%). Also the founders’ personal stake are quite important: Robert Kotick (0.55%) and Brian Kelly (0.68%).

Let’s take a look at Activision Blizzard’s Financial Statements to see if it is an adequate company for our DGI strategy.

1) FINANCIAL HEALTH: Balance Sheet

Activision Blizzard’s Balance Sheet is surprising at first glance because of its large Equity and its enormous Cash. Let’s take a closer look.

Short-Term Assets and Liabilities

Activision Blizzard’s Liquidity Ratio and Cash Ratio are impressive: 5.21 and 4.32 respectively. We have rarely seen such high liquidity ratios on our blog. As we will see below, this company is a great cash generator. And since it pays a very modest dividend and does not usually make major acquisitions on a recurring basis, it accumulates cash on its balance sheet year after year.

To picture this, Activision Blizzard could pay almost 2 times all its short and long term Debt only with the money it has in Cash. Moreover, the cash they have (more than $10.4 billion) is so large that, if we assume that the company should have a Liquidity Ratio of 1, then the excess cash would represent almost $13 per share. At current prices, that is almost 18% of its share price, simply amazing.

Therefore, not only can we say that Activision Blizzard’s short-term Balance Sheet is tremendously strong, but we should also try to understand why this excess cash is not invested in some income-generating asset. The most likely explanation is that this cash accumulation is intended to make it more difficult for other companies to acquire Activision Blizzard. After Microsoft’s acquisition announcement, it would be possible for other companies to join the bidding. But having a lot of cash on hand makes the deal more expensive for buyers, which is partly why Microsoft has not yet encountered competition in the bidding for Activision Blizzard.

Long-Term Assets and Liabilities

As we have already seen, Activision Blizzard has negative Net Debt: -2.02 times EBITDA. Moreover, the average interest rate on debt is less than 3% and it does not have to repay more than half of it in 25 years. Therefore, it is not even in Activision Blizzard’s best interest to repay what little Debt it has.

On the other hand, the Financial Autonomy is huge: 70%. Activision Blizzard carries some Goodwill on the Balance Sheet as a result of its historical acquisitions, but even if we were to remove it from the Balance Sheet, the Financial Autonomy would still show a reasonable value: 31%.

Therefore, we can affirm that Activision Blizzard has a very robust Balance Sheet, which provides it with an enviable Financial Health.

2) PROFITABILITY: Income Statement 2021

Sales

Activision Blizzard’s Sales have grown by a remarkable average of 6.35% per year over the last 10 years. In 2017 we appreciate a sharp drop in Net Profit, which is the result of the one-off adjustment caused by Donald Trump’s US Tax Reform Act.

Activision Blizzard’s sales are largely due to its flagship games: Call of Duty, World of Warcraft and Candy Crush. Between them, they represent 82% of the sales of the entire company. Moreover, these 3 video games increasingly weigh more and more on Activision Blizzard’s Sales: in 2019 they only accounted for 72% of the total.

As we have already seen, 74% of sales are due to subscriptions, in-game purchases for additional benefits or accessories, and by licensing to other companies. All this is called «In-Game» sales. The traditional business of selling video games now only represents 24% and is decreasing every year. What’s more, in-game micro-transactions from players alone, in the form of downloadable content and in-game perks, already account for almost 60% of the company’s sales. That is why it is so attractive for a company like Microsoft to incorporate into the subscription service of its cloud platform a series of video games like these, which generate their sales in a recurring and online way.

Sales are well distributed in terms of devices played on, and given the importance of In-Game Sales, one of the most important parameters to analyze is the MAU: Monthly Active Users. This gives us an idea of the success of Activision Blizzard’s games and their trend over time.

Last year has seen a decline in MAUs (-6.5%), mostly in the Activision division, due to a decline in Call of Duty players. Blizzard division has also fallen in MAUs, and King division has held its own. However, despite the decline in MAUs, Sales are up 8.9% due to higher Sales in Candy Crush content and advertising, and a positive impact from the USD exchange rate in 2021. It’s yet to be seen if in the future the new versions of Call of Duty and Warcraft manage to convince more players by increasing their MAUs.

On the other hand, it is remarkable that the Asia-Pacific region only represents 12% of the company’s sales. This region of the world has an enormous potential in the video game sector, although it presents hard complications for foreign companies that want to operate there. Especially in countries like China, which is why Activision Blizzard had entered the market with Netease. Let’s hope that the termination of their agreement will turn into a new one with Netease or with any other company, since the growth potential in this geographic area is very high.

Another point to highlight in Activision Blizzard’s sales is that the other large companies of the video game sector are Activision Blizzard’s main clients. Activision Blizzard is paid through the platforms of these large companies, where their customers buy the games. For example, Sony and its Playstation console accounted for 15% of Activision Blizzard’s sales last year. Apple and Google also represent 17% each, and Microsoft is close to 10%. Undoubtedly, these are very interdependent companies, and that is why Sony is now putting all possible obstacles to the acquisition of Activision Blizzard by Microsoft.

In its Q3 2022 results, Activision Blizzard indicates that it expects to end the year with -5% in Sales. This is due to several factors. On the one hand, 2021 confinements caused a boom in the video game sector that is slowly moderating as the pandemic is left behind. On the other hand, Sales have fallen by almost 22% in the first 9 months of 2022 mainly due to the Activision segment, given that the new «Call of Duty: Modern Warfare II» was not launched until October 28th. It seems to be the most successful edition of this franchise in terms of sales on its release to date. But the reality is that, as of Q3 2022, the Activision segment had reduced its revenue by 38% from the previous year. In addition, the currency exchange rate has negatively affected the current fiscal year. Anyway, the company expects to cushion this drop to an overall (-5%) thanks to the new Call of Duty, the better performance of Blizzard and especially King and its Candy Crush, which is targeting a +8% in Sales in 2022 compared to the first 9 months of 2021.

Margin

Activision Blizzard has an extraordinary Net Margin of 31% in 2021. This is the highest Net Margin in the last decade, although since 2018 the average is at 26%. Undoubtedly a very high value.

To put it in perspective, its closest competitor, Electronic Arts, has a Net Margin of about 10%. The one of its former partner Netease is under 20%, and Ubisoft is under 5%.

In addition, the 3 divisions (Activision, Blizzard and King) all have very good Operating Margins, with Activision (Call of Duty) standing out above the others with 47%.

Sankey Chart

Profitability Ratios

ROA: 11% (Net Earnings/Total Assets)

ROE: 15% (Net Earnings/Equity)

ROCE: 30% (EBIT/(Equity + Net Debt))

Activision Blizzard’s Profitability Ratios are spectacular.

The ROA of 11% indicates that despite having a significant amount of Goodwill on the Balance Sheet and a huge amount of Cash, the company still makes a lot of money on its Assets. If the company had less Goodwill and less Cash, this ratio would be even higher. This high ROA also indicates that Activision Blizzard needs to invest very little to obtain a high return.

On the other hand, both ROE and ROCE show very high values, especially with such a high Financial Autonomy (70%).

In short, these excellent profitability ratios confirm that this is an excellent business.

Earnings per share (EPS)

Earnings per share have grown even more than sales: an annual average of more than 14% over the last decade. This is partly explained by the large number of Share Repurchases the company has made. The chart clearly shows the effect of Donald Trump’s US Tax Reform Act in 2017, and the effect of the King acquisition from 2018.

In the next fiscal year we will undoubtedly see a reduction in EPS due to the expected drop in sales. This fall may be quite accentuated in the EPS, given that the company’s personnel, development and distribution are largely fixed costs, whether or not the new editions of videogames are successful. We will see if the launch of «Call of Duty: Modern Warfare II» manages to recover the company’s earnings per share, which in the first 9 months of 2022 had fallen by 48% compared to the first 9 months of the previous year.

3) DIVIDEND

Dividend per Share (DPS)

Activision Blizzard paid its first dividend in 2010. Since then, it has increased it gradually until 2020, at an average annual rate of 12%. However, in 2021 it has not increased it any further, due to the announcement of acquisition by Microsoft.

If we had purchased Activision Blizzard stock in 2016 at $36, in 2021 we would have a Dividend Yield of 1.3%.

If we had bought in 2011 at $12, in 2021 our Dividend Yield would be 3.9%.

Currently, the initial Dividend Yield is around 0.6%, a very low one. Even with a fairly high dividend growth, we would have to wait a long time to have a considerable dividend yield. However, as we will see below, the company could afford to raise the Dividend quite a bit, which it has not yet done due to the acquisition announcement by Microsoft.

Payout (Dividends/Net Income)

Activision Blizzard’s payout is very low, barely 14%. Historically it has been approximately 15% to 20%, so it has plenty of room to increase it in the future.

Cash Flow

Cash Flow – Maintenance CAPEX

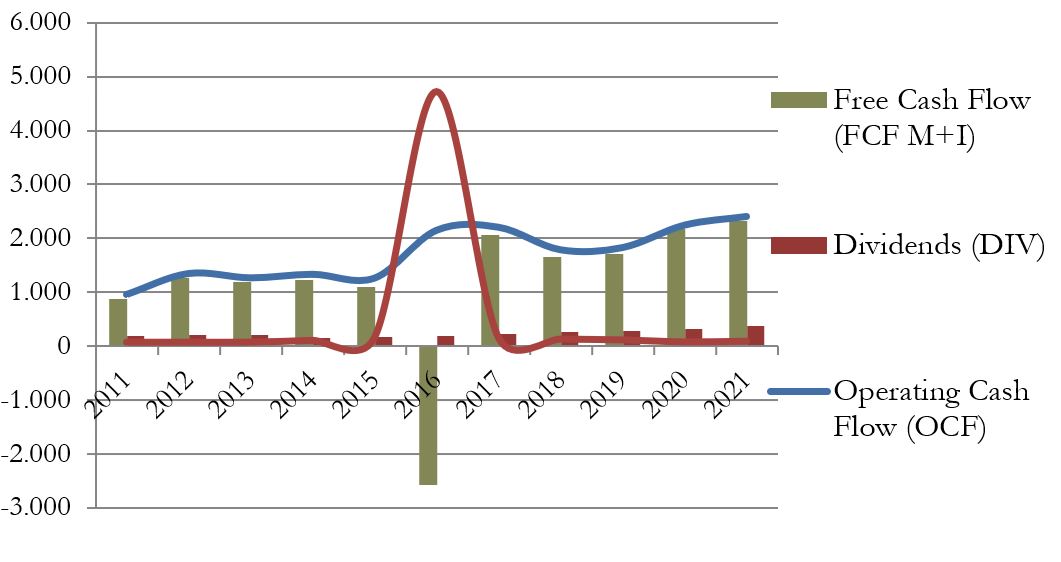

The Cash Flow chart considering only the Maintenance CAPEX is perhaps the best indicator of all this analysis, as to the quality of Activision Blizzard’s business.

On the one hand, even with ups and downs, Operating Cash Flow is growing strongly, multiplying by 2.5x in 10 years.

But most impressive of all is how little Maintenance CAPEX the company needs to generate such a high OCF. Maintenance CAPEX is so low that Free Cash Flow is tremendously high and growing. Moreover, dividends are only a fraction (about 15%) of this FCF.

Without a doubt, Activision Blizzard is a cash-generating machine, and the dividends it pays out are more than sustainable: there is still plenty of room to increase them.

Cash Flow considering CAPEX of Total (Maintenance + Investment)

If we take into account the Capex of Maintenance + Investment, we appreciate very clearly the huge amount due to the acquisition of King in 2016.

However, this large outlay, which we understand is necessary in the business to remain at the forefront of the video game industry, does not represent more than 2 times the Free Cash Flow of the last year.

This confirms that Activision Blizzard is an excellent cash generator, and an extraordinary business.

Share Repurchases

Activision Blizzard today has 32% fewer shares than in 2011, largely due to moves by former large shareholders such as Vivendi. However, since 2014 the number of shares has remained more constant, increasing slightly year-over-year due to share-based payments to certain employees (approximately +1% annually). To offset this shareholder dilution, Activision Blizzard approved the repurchase of $4 billion in shares in early 2021, approximately 7% of capitalization at current prices. However, these buybacks did not take place and have been put on hold, waiting for the outcome of Microsoft’s attempted acquisition.

Conclusion

Today we have seen an excellent company, with a very robust balance sheet, a lot in cash, and still with excellent profitability ratios. In addition, it belongs to a sector that grows considerably and is coveted by large corporations such as Microsoft.

The dividend has always been small, although it has increased at a good and sustainable rate until the company decided to freeze it waiting for the outcome of Microsoft’s takeover attempt.

Moreover, it is a company that has revolutionized the world of video games and has become the main game supplier of major global companies such as Sony, Apple, Google or Microsoft thanks to its franchise games that are updated and improved year after year.

Even Warren Buffett has decided to become its largest shareholder at $77 per share, despite not yet knowing whether global regulators will allow Microsoft’s acquisition. Therefore, one can imagine that the Oracle of Omaha would not be averse to keeping the stock at $77 per share either, which would actually be $64 per share if we discount the company’s excess cash: a P/E of 18.6 based on 2021 EPS and about P/E 25 based on expected EPS for 2022. It would not be a very cheap price, but if we consider that on the other hand he would have a profit of $18 per share if the acquisition is completed, it does not seem a bad deal at all.

At Dividend Street, we believe that on its own, Activision Blizzard is a company that could fit in our personal portfolio for our very long-term strategy. It is certainly not a cash cow, nor is it one of the fastest dividend growers. But it does pay out a dividend that has so far been growing and sustainable. In any case, the truth is that its main attraction lies in the arbitrage operation that could occur if Microsoft ends up acquiring the company: a 30% revaluation to current price in just a few months.

What do you think of Activision Blizzard? Do you hold it in your portfolio? Does it seem an interesting stock to buy? Is it suitable for your strategy?

If you would like more details on historical data or target prices, the Report is at your disposal.

We hope you liked the analysis. We encourage you to upload your comments and share the article on Twitter. For those who visit us directly, we leave you the subscription link in case you do not want to miss any of our articles.

Also, ¡never forget to make your own analysis before taking any investment decisions!

Best regards and see you in the next article!

Sources consulted:

Annual Reports (2011-2021) Earnings Q3 2022 www.fundinguniverse.com https://portal.33bits.net/activision-la-primera-third-party/ https://en.wikipedia.org/wiki/Activision#Early_years_(1980%E2%80%931982) https://www.activision.com/company/aboutus https://en.wikipedia.org/wiki/Bobby_Kotick https://www.fool.com/investing/2020/02/18/if-invested-10000-activision-blizzard-

ipo-how-much.aspx https://es.wikipedia.org/wiki/Activision_Blizzard https://www.marketscreener.com/business-leaders/Robert-Kotick-3344/biography/ https://www.sec.gov/Archives/edgar/data/718877/000130817921000289/latvi2021_defr14a.htm https://www.levelup.com/noticias/655348/Mujeres-de-Treyarch-alzan-la-voz-sobre-los-problemas-de-ActivisionBlizzard https://www.eleconomista.es/mercados-cotizaciones/noticias/11493314/11/21/Game-over-para-Bobby-Kotick-el-rey-de-los-videojuegos-que-esta-en-apuros.html https://en.wikipedia.org/wiki/Video_game_publisher#Major_publishers https://markets.businessinsider.com/news/stocks/warren-buffett-berkshire-hathaway-unaware-microsoft-takeover-activision-blizzard-st https://markets.businessinsider.com/news/stocks/warren-buffett-berkshire-hathaway-unaware-microsoft-takeover-activision-blizzard-st