Dear readers, let´s analyse the last annual results of the aristocrat VF Corporation, a company that manages the iconic brands of Vans, The North Face, Timberland and Dickies among others. 48 consecutive years of dividend increases endorse this company for our DGI strategy.

INTRODUCTION

Origins

In 1899, eight partners created the textile company «Gloves and Mitten Manufacturing» in Reading, Pennsylvania. Among them was John Barbey, an engineer and businessman who had no previous experience in the textile sector. However, he was a skilled businessman who had been previously involved in the brewing beer business with his father, and had already worked in various financial institutions in Reading. He therefore took charge of the company’s finances and after 12 years decided to acquire the shares of his partners. It was 1911.

After a while, Barbey decided to expand the company’s production by manufacturing silk lingerie. This type of lingerie was usually marketed without any brand, and John Barbey wanted to give the lingerie a commercial brand well-known and appreciated by its customers. In order to do this, he started a company division in 1914 called «Vanity Fair Silk» with a major advertising campaign to publicize the benefits of quality and style that the Vanity Fair lingerie provided. He even went so far as to change the company’s name to Vanity Fair Silk Mills, Inc. in 1920. In the early 1920s, the growing success of the intimate apparel product line led the company to discontinue its glove manufacturing operation and focus exclusively on the lingerie business.

In 1939 John Barbey died, and difficult times began: in 1941, World War II led to a silk embargo, and the company began using rayon in production. The silk embargo led the company to drop the word «Silk» from the corporate name in 1942. During the rest of the decade, Vanity Fair perfected the use of new types of fabrics and later introduced lingerie products made of a new material: nylon tricot. This material was soon considered the ideal lingerie fabric because of its strength and elasticity. Its use also enabled the company to produce lingerie in many colors.

In 1951 Vanity Fair Mills was listed on the New York Stock Exchange and continued to focus on the lingerie business for two decades. In 1969 Vanity Fair began its evolution into a multi-brand apparel company by acquiring the famous Lee Company brand of jeans and pants. After this acquisition Vanity Fair changed its name to VF Corporation.

Due to the growing demand for jeans, Lee became VFC’s largest operating division, accounting for up to 80% of the company’s revenues in the late 1970s. Although the denim market was declining in the 1980s, VFC was much better positioned than its competitors Levi’s and Blue Bell due to greater diversification.

The next major milestone came in 1986 with the acquisition of Blue Bell, a competitor that was the producer of Wrangler jeans as well as other brands such as Rustler, Jantzen and JanSport swimwear and sportswear, and Red Kap workwear. After the addition of Wrangler, VFC became one of the two largest jeans producers in the world with a 25% market share. The other major denim producer was Levi’s.

Since the beginning of the 21st century, VFC has experienced a real revolution: in 2000 it bought The North Face Inc ($310M), in 2004 Vans ($400M), in 2011 Timberland ($2,000M), in 2017 Williamson Dickie ($820M) and in 2020 Supreme ($2,100M). These acquisitions now represent the company’s top 5 brands. In this period it has also bought other important brands such as Eastpak, Kipling, Napajiri or Icebreaker.

On the divestment side: in 2007 they divested Vanity Fair (the underwear brand that had been part of the company since its creation), between 2017 and 2018 they sold the Majestic and Nautica brands, and in May 2019 they spun off their Jeans division, which housed two of their most iconic brands: Lee and Wrangler, which were separated into a new company called Koontor, listed on the New York Stock Exchange under the ticker $KTB. The Spin-off was completed on May 22, 2019 by distributing 100% of the shares of Kontoor Brands to VFC shareholders. They received one share of the new Kontoor Brands stock for every seven shares of VFC.

Finally, in 2021, VF decided to sell all of its Work brands, except Dickies and Timberland Pro, to a subsidiary of the asset manager Redwood Capital Investments for approximately €605M. There are currently 13 brands marketed by VFC. We will now take a closer look at them.

Business

VFC is one of the world’s largest apparel, footwear and accessories companies, and stands out for its great adaptability in building its brand portfolio. Despite having reduced the number of brands (and thus diversification) in recent years, the brands operated by VFC are highly recognized.

VFC is divided into 3 business segments:

- Outdoor: Sports and casual clothing, footwear and accessories for outdoor and mountain activities.

- Active: Urban footwear and clothing, and backpacks. Focused on a younger audience.

- Work: Workwear, this segment has been reduced to only Dickies and Timberland Pro brands.

Brands and sales are structured as follows:

Outdoor and Active account for 90% of turnover. Direct Sales are also increasing, to the detriment of Wholesales: VFC is focusing on offering a more personalized treatment to customers through digital sales and its own stores. The sale of its workwear segment (excluding Dickies and Timberland Pro) reaffirms the strategy of further simplifying the operating model to focus on consumer and retail. Geographically Sales have some dependence on the USA, but are reasonably diversified, and currently the fastest growing regions are APAC and EMEA.

Analyzing the brands, VFC details only the revenues of Vans, The North Face, Timberland and Dickies. Sales of the Big 4 brands represent 69% of VF’s global sales, a weight that has been somewhat reduced following the purchase of Supreme in 2020.

With so much diversification, it is difficult to determine VFC’s competitors: in Active, the most direct competitors are Nike and Adidas, while in the Outdoor segment, Columbia and Patagonia compete with The North Face, and Tommy Hilfiger and Hugo Boss compete with Timberland.

Vans, Timberland and Supreme are more linked to the fashion world, a very competitive sector due to the lack of differentiation and the continuous change of trends, which has historically grown at rates of 4-6%. The North Face is more focused on sports and outdoor gear, a booming industry with high growth expectations thanks to an increasingly health-conscious population and the growth of emerging markets, which are already a considerable market. As a result, this brand has been performing very well in recent years.

Although VF does not have such a wide moat based on a single brand as Nike and Adidas, the future of these companies is tied to the future of their brand name. In contrast, VF is highly adaptable, as it has based its strategy on focusing on brands with better margins and prospects. In recent years VFC has not hesitated to divest brands of its portfolio that weren’t profitable enough anymore.

VFC’s strategy is to buy competitor’s brands if it finds opportunities; it is also inclined to expand its sales in the Asia-Pacific region, especially in China, where sales have historically grown at high rates, even if they have stagnated a bit since the pandemic. At the same time, it wants to boost direct-to-consumer sales, especially through Internet sales.

Analyzing the main shareholders, we find a fairly concentrated participation, as 50% of VFC shares are distributed among 6 shareholders: Capital Research & Management owns about 15% of the company, The Vanguard Group and PNC Bank each have a 10% stake, followed by Northern Trust Investments (6.42%), Todd Barbey (5.16%) and State Street (4.66%). Among these investors, the large stake of private investor Todd Barbey (a descendant of VFC’s founder) stands out, and it is estimated that the Barbey family owns around 17% of the listed shares.

1) FINANCIAL HEALTH: Balance Sheet

Despite having a positive current ratio, the composition of the Balance Sheet seems a bit fragile: Debt is starting to pile up and Intangible Assets are higher than Equity.

Short-Term Assets and Liabilities

In 2022 the Liquidity Ratio shows a value of 1.45 and the Cash Ratio stands at 0.38. We normally consider these ratios to be prudent values for the short term, but it is worth mentioning that the Liquidity Ratio shows a lower value than in previous years, and that a large part of the current liabilities is Financial Debt.

On the other hand, the cash conversion cycle (92 days in 2022) is quite high, which forces the company to keep money in cash in order not to have any setbacks: the collection period from customers (43 days) is longer than the payment period to suppliers (35 days), and the inventory conversion is also quite long (84 days).

Therefore, although at first glance they appear to be prudent values, the reality is that the ratios in the short term are a little tight, given the management of working capital.

Long-Term Assets and Liabilities

In the long term we see high Intangibles and Goodwill. Together they represent 40% of Total Assets, due to the company’s inorganic growth policy. All this despite having impaired $1,300M of Goodwill since 2010. The last impairment charge was made in 2019 for Timberland brand ($323M).

Financial Autonomy has been greatly reduced in 2022. Net Equity represents 26% of Total Assets while in 2010 it represented around 60%. The company’s equity has shifted from Retained Earnings (which have also been deteriorating) to Financial Debt. Supreme’s most recent acquisition in 2020 ($2,100M) was mainly financed with Debt. So we see a decreasing Financial Autonomy due to being financed with more and more debt.

However, the average interest rate of all Debt is 2.05%, which is much lower than its ROA. It seems that the Financial Debt is not yet a danger for VFC’s solvency despite the fact that more than half of it has a maturity of less than 5 years. This is due to the low interest rates and the fact that the Net Debt/EBITDA ratio is around 2, a high but still manageable value.

2) PROFITABILITY: Income Statement 2022

Sales

VFC’s sales have been stagnant for a decade, largely due to the spin-off of the jeans segment which accounted for almost 20% of the company’s global turnover. The acquisitions of Dickies and Supreme since 2012, do not compensate for the spin-off of Kontoor and the large divestment in the Work segment. It is worth mentioning that VFC changed the end-date of its fiscal year in 2018 and therefore the chart is distorted that year.

After some troubled years marked by the pandemic, the spin-off of Kontoor and the sale of a large part of the Work segment, Sales seemed to be back on track in 2022 and results were positive in virtually all brands and segments of the company. The North Face brand has stood out, which has been growing rapidly over the last few years thanks to international momentum and growth through retail (DTC) and digital channels. However, Sales continue to stagnate in APAC, especially in China, a region that historically grew at double digits and where Vans’ sneakers sold very well.

In Q1 2023 Sales increased by +3% compared to Q1 of the previous year. These is lower than expected growth due to an unexpected decline in the APAC region, the appreciation of the dollar (which is bad news for exports) and increasingly widespread sentiments of a future recession. Because of all these issues, 2023 Sales growth guideline has recently been reduced to ranges between 5-6% from previous 7% expectations.

Margins

In 2022 the Operating Margin amounted to 14%, while the Net Margin stood at 12%, correct margins and somewhat higher than the rest of the companies in the sector, demonstrating some pricing power. Looking at margins by division, the Active segment is the most profitable, although all segments in general report good margins.

If we compare the Active segment with Nike and Adidas, Active’s operating margin is higher than that of these two iconic brands, while the Outdoor segment is at similar values to those of the main competitors.

Although Sales are still expected to increase by 2023, Gross Margin has been sharply reduced in the first two quarters (from 56.5% in 2022 to around 53.5% in 2023). It seems that VF has not been able to incorporate inflation to its prices. And it may have to apply discounts to many garnments not to accumulate too much stock. This is mainly due to the appreciation of the dollar.

The fact is that the company expects to report an Operating Margin of 12% for the year 2023 (two points below the previous year). However, given the current situation of uncertainty, a drop of 2 points does not seem too drastic, and we are confident that in the medium term VFC should be able to keep its pricing power.

On the other hand, in Q2 2023 the company will report losses between $300M and $450M to the impairment of the Supreme brand, so the Net Profit expectations for next year are not flattering, and Earnings per Share are expected to be down -17% in 2023 compared to the previous year. These extraordinary losses should not be too alarming, but it is worrying to see that this recent investment is not generating the expected returns yet.

Sankey Chart

Profitability Ratios

ROA: 10% (Net Income/Total Assets)

ROE: 39% (Net Income/Equity)

ROCE: 22% (EBIT/(Net Equity + Net Debt))

In 2022 the ROA stood at 10%, a value that justifies the Intangibles VFC has in its Balance Sheet and well above the interest they pay on Debt.

ROE and ROCE are considerably high, despite the reduced Financial Autonomy, we are reassured to see a high ROCE.

However, given that Net Profit fluctuates a lot over the years, the data on margins and profitability ratios should be taken with a pinch of salt.

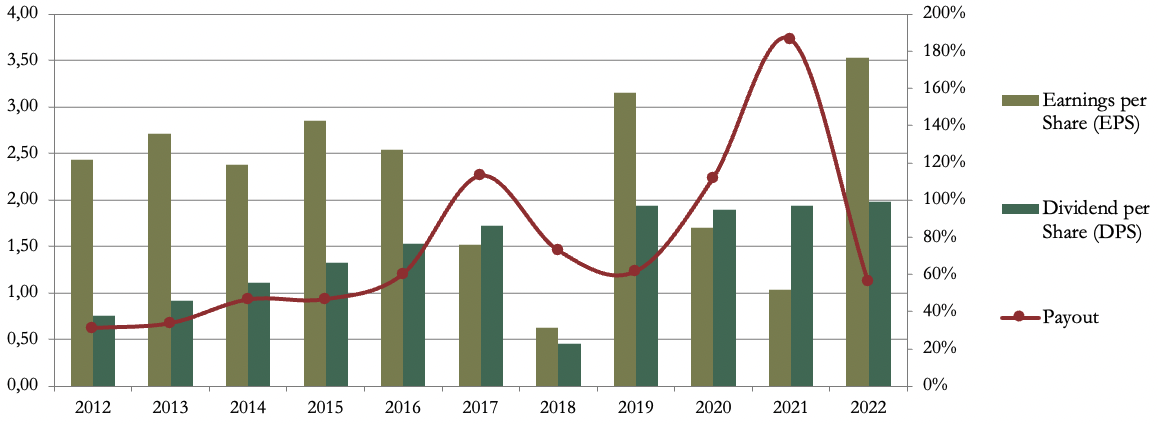

Earnings per Share (EPS)

Despite the many ups and downs of recent years, EPS has grown by an average of 3.8% per year over the last decade. Fairly moderate growth, thanks to a slight increase in margins, and despite sales remaining flat due to divestments in less profitable brands. EPS has been boosted by the generous share buyback policy carried out over the last few years.

After the first two quarters of 2023, the company has reduced the EPS guideline estimating a decrease of around -17%, due to a reduction in margins, and especially because of the impairment of Supreme discussed above.

3) DIVIDEND

Dividend per Share (DPS)

With 48 consecutive years paying growing dividends, VFC is on its way to becoming a Dividend King. Moreover, if we analyze the last ten fiscal years, the Average Annual Growth (10%) has been considerable. But it is worth mentioning that the growth from 2012 to 2017 was 18% per year, while since 2019 it has been growing at a rate of 2% per year.

At current prices at the time of writing, VFC is paying an initial dividend yield of around 6% , a historically very high dividend yield (DPS) for this company.

If we had purchased VFC stock in 2017 for $53, we would now have a 3.77% dividend yield.

Had we done so in 2012 for $32, we would now have a 6.25% dividend yield.

Looking at the historical share price, shareholders who bought shares from 2014 onwards must not be very happy at present. VFC is not going through its best cycle.

Payout (Dividends/Net Income)

Payout oscillates a lot due to the irregularity of VFC’s results. However in a good year like 2022 it reached 56%. This is a higher than usual value, but still sustainable and in line with the Payout that the company expects to have in the coming years.

Cash Flow

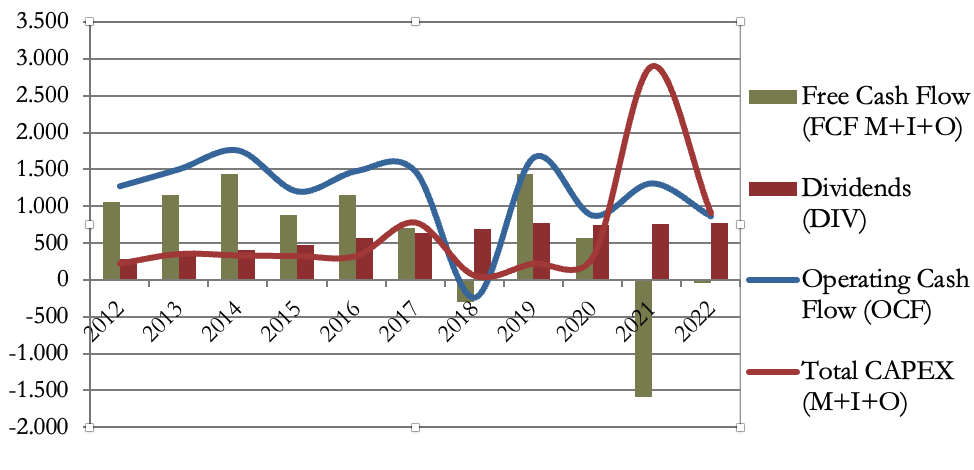

1) Cash Flow – Maintenance CAPEX

Despite VFC’s strategy to optimize its brand portfolio, the reality is that Free Cash Flow has shrunk over the last decade. Especially since COVID 19, from which it seems that VFC has not yet fully recovered.

VFC’s Operating Cash Flow has many ups and downs due to working capital management which tends to change +/- $400M depending on the year. All in all, we see a decreasing OCF trend and an increasing Maintenance CAPEX, and consequently the FCF has been reduced quite a bit over the last decade. It appears that the business is suffering from temporary problems since the pandemic.

2) Cash Flow – Total CAPEX

If we take into account the Investment CAPEX, the results are not very flattering either. In recent years, there has been a clear shift from Kontoor (2020) and most of the Work segment (2022) to buy the Supreme brand (2021).

Probably shareholder remuneration will grow at a slower rate over the next few years, as it is unsustainable to continue with the increase it at this rate. Over the last decade VFC has paid out more cash to shareholders than it has actually generated. By our calculations, from 2012 to 2022 VFC has generated Maintenance + Investments FCF of $9,515M while it has paid out $11,633M to its shareholders if we add Dividends to Share Repurchases. Not surprisingly, Financial Debt has increased.

Share Repurchases

VFC is prone to share buybacks, and does so fairly regularly reducing the number of shares outstanding by an annual average of 1.25% over the last decade. This has undoubtedly helped EPS to grow slightly over the last decade despite divestments.

In FY2022 VFC repurchased $350M worth of shares at an average price of $72.84, which is a very high price. We don’t like to see VFC buying back its own shares on inertia, even when their share price is high. But as are still $2,500M approved for future buybacks, it will be interesting to see if the company takes advantage of the current low prices to make some significant buybacks, and if in doing so it demonstrates confidence in its own business.

Conclusion

There is no doubt that VFC has highly recognized brands and a significant diversification that has allowed it to focus on the most profitable brands with the best growth prospects. This portfolio optimization has caused sales to remain flat over the last ten years, but there has been a slight increase in margins.

The composition of the Balance Sheet has deteriorated over the last few years: working capital management is far from good, Intangibles and Financial Debt have increased and Financial Autonomy is decreasing, as in recent years VF has paid back to shareholders much more than it has generated. All in all, the Balance Sheet is not yet in alarming ranges, although we would like the company to improve in this aspect.

Since the Balance Sheet situation is not yet alarming and VF is a company that is very committed to paying Dividends, we do not believe that management is considering cutting it. However in recent years DPS has grown much more than EPS, and the company has paid out much more in Dividends and Share Buybacks than FCF it has generated, so it seems that this growth will at least be much slower in the future.

VFC has a good business, but it is going through temporary problems due to an irresponsible period of shareholder remuneration, and also to a poor performance of Cash Flow since the pandemic started. Therefore, although the initial dividend yield is currently attractive, we do not expect very high dividend growth over the next few years.

What do you think of VFC? Do you have it in your portfolio, and do you see it as a good investment opportunity at this time?

If you would like more details on historical data or target prices, the Report is at your disposal.

We hope you liked the analysis. We encourage you write a comment and share the article on Twitter. For those who visit us directly, here is the subscription link if you don’t want to miss any of our articles.

Best regards and see you in the next article!

Sources consulted:

Annual Reports 2011-2022

http://www.fundinguniverse.com/company-histories/vf-corporation-history/

https://www.vfc.com/our-company/company-history

https://www.vfc.com/investors/financial-information/earnings-results

https://seekingalpha.com/article/4502307-vf-corp-stock-smart-bargain-dividend- investors

https://seekingalpha.com/article/4519455-vf-corporation-mr-market-is-probably-right

https://seekingalpha.com/article/4543880-vfc-stock-uncrowned-dividend-king-value- trap